If as a non resident you own a Spanish property that is for for personal use and NOT let out at all it is liable to pay tax called Renta Imputada – Deemed Income tax declarable on a form called Modelo 210.

If your property is left empty, even though you do not let out your holiday home for gain, Spanish law assumes you have what is called a “Deemed (Rental) Income” which is subject to non-resident Income Tax.

The “Deemed (Rental) Income”, which historically was included on the old Modelo 214 form, is now declared on a Modelo 210 form. In 2011 the format of this form changed to be more user friendly, being reduced from 7 pages to 3!

However the authorities are cramming a lot more into those three pages than they used to! The following information is now obligatory for ALL owners:

- National Insurance number in your country (if you are reading this site probably the UK)

- Spanish NIE number

- Passport number

-

Date of Birth

-

Town of Birth (as per your passport)

-

Country of Fiscal residence (probably UK but needs to be confirmed)

-

Address in your country of residence (probably but not necessarily the UK)

- Full Address of the property or properties in Spain

- Catastral Value and year revised

-

Catastral reference number of Property in Spain (shown on the IBI bill)

-

An IBAN bank account number to include on the form if you want to pay from your bank.

The form CAN ONLY be completed on line at the Tax Agency’s website There are currently (2022) 2 versions, one for the tax years 2011 to 2017 and another for tax years from 2018 onwards.

If you are unable to speak Spanish we offer an interpreting service to help you to self-assess these Deemed income tax returns at 67,50 euros per property per year as long as the property is owned by between 1 and 3 people, as a return is required for each owner of the property. If you let out for gain (see here) please contact us to ask for detailed information.

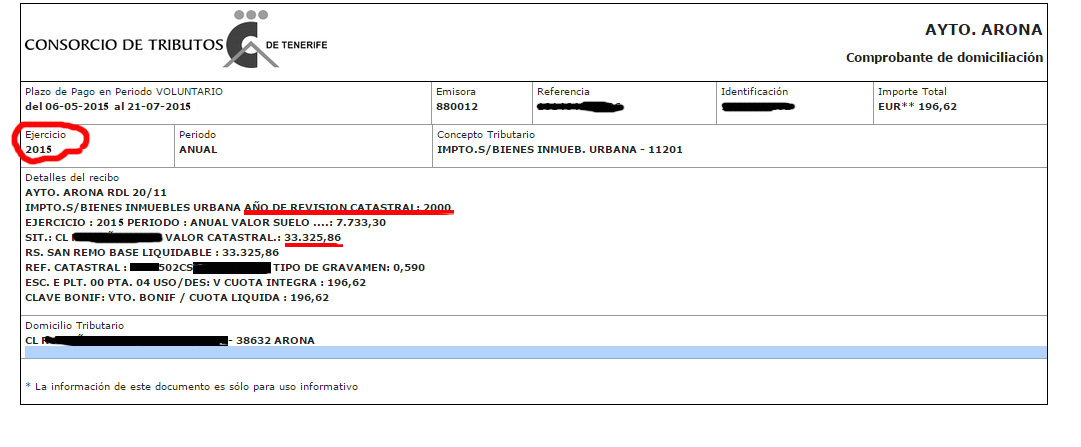

The amount you pay is calculated using the “Valor Catastral” (Rateable Value) of your property in Spain. This can be easily ascertained by looking at the receipt for your “Impuestos Sobre Bienes Inmuebles” or IBI, (often referred to by English speakers as “Rates”) – which is paid to your “Ayuntamiento” annually.

|

Non Residents Tax – Changes to information available on IBI Bills As some of you may have noticed if you pay your “Impuestos Sobre Bienes Inmuebles” (local authority rates) through your bank they are no longer giving full details on the bank slips. If you pay your “Ayuntamiento” directly in their offices annually you will receive a receipt with all the information you need. If you pay by direct debit and your Ayuntamiento uses the Consorcio de Tributos de Tenerife to collect this on their behalf you can go on line and access a copy of the IBI receipts showing the full information. More information HERE If your local authority does not use Consorcio (such as Adeje) then it may be helpful to make a trip to your town hall to ask for a printout, there is also an online system for Adeje see HERE . In the past the rateable value of your property would have been clearly shown on your IBI receipt, this is the base used to calculate the amount due on the 210. Since 2015 the method of calculating which percentage to be used changed. If the revision date is over 10 years then the base is 2% and if it less than 10 years then its 1,1%. |

The actual tax payable on the “Deemed (Rental) Income” derived using the coefficient is……..

Remember the tax is payable a year in arreas.

From 2015 onwards the tax payable is:

- Contributors who are fiscally resident in the EU, Iceland and Norway: 19%

Rest of contributors 24% (from 2021 onwards the UK tax residents are considered non-EU so will pay 24%)

The deadline for the submission of form Modelo 210 is the 31st December each year for income deemed or actually derived in the previous year unless you have more than one property in which case the deadline is the 30th June of the following year.

All of the above applies to Non-residents with no permanent establishment but who own a holiday home in Spain.

An example of a receipt for “Impuestos Sobre Bienes Inmuebles” or IBI is shown below (obviously you will need to obtain the most recent one each year to spot changes to the valor catastral): The format can vary between Ayuntamientos, or whether you get the receipt direct from the Ayuntamiento or from the Consorcio system. But all the information you need will be on there.

Based on the receipt below here are some examples of a calculation of the tax due for the 2020 tax year payable up to Dec 2021 :

| Tax Year 2020 – EU resident | Tax Year 2020 – EU resident | Tax Year 2020 – NON EU resident |

| Catastral revision Year 2000 | Catastral revision Year 2016 | Catastral revision Year 2000 |

| 2020-2000=20 ie MORE than 10 years | 2020-2016=4 ie LESS than 10 years | 2020-2000=20 ie MORE than 10 years |

| So coefficient in this case is 2% | So coefficient in this case is 1.1% | So coefficient in this case is 2% |

| Catastral Value is 33,325.86 | Catastral Value is 33,325.86 | Catastral Value is 33,325.86 |

| Caculation: | Caculation: | Caculation: |

| 33,325.86 x 2% x 19,0% | 33,325.86 x 1.1% x 19,0% | 33,325.86 x 2% x 24% |

| Tax to declare on modelo 210 = 126 euros 64 cents | Tax to declare on modelo 210 = 69 euros 65cents | Tax to declare on modelo 210 = 159 euros 96 cents |

New for 2020 is an extra button on the form which will auto calculate the Base imponible (taxable base figure) for you as long as you have the above information to hand.

New for 2021 payable 2022: Due to the UK’s withdrawal from the EU at the end of December 2020 UK residents who are Spanish NON resident tax payers will have to calculate using the 24% higher rate for NON EU residents.

Do you know someone who has owned property for years and never made a declaration? Probably. However, if they are caught, and computerised records are making that ever more likely, they are liable to pay the last four year’s tax and probably a hefty fine. This articles aim is to make non-resident homeowners aware of their legal obligation to submit an annual income tax declaration in Spain; it is not intended to be a crash course on Spanish tax law. This is a complicated subject and people’s circumstances differ. But what holds true for all, is that no non-resident home owner, whatever their circumstances, is exempt from making a non-residents Income Tax return and you should always check your particular circumstances with a tax professional.

But in any case whether you receive a demand letter or when that property is eventually sold or passed on as part of an inheritance, the Spanish Tax Agency can and will check their records, which will show the property is owned by a non-resident and that no tax declarations have been received. The non residents taxes will then need to be paid, including any fines imposed, before the property can be legally transferred, or before any rebate due of monies retained against capital gains can be made.

At The One Stop Problem Shop we can assist with preparing and presenting this tax. Please get in touch using the links below if you require our assistance.

Contact Us

📩info@theonestopproblemshop.com

![]() WhatsApp 659719695

WhatsApp 659719695

📞 922 783828 or 659719695